|

Bold ideas that solve the world’s energy needs.

|

The New Frontier: The Opening of the African Oil and Gas Industry

by Anton Botes, Andrew Lane, Hannah Edinger

|

Bold ideas that solve the world’s energy needs.

|

|

In 2000, The Economist dubbed Africa ‘hopeless’. Over the next decade, Africa rebutted that tag: labor productivity rose, inflation dropped and economies boomed. The Economist positively revised its opinion of Africa in 2011. Three years later, a crash in oil prices changed that upbeat narrative with a devastating economic blow to African oil-producing nations. Economies have slowly recovered and Africa’s gross domestic product (GDP) growth is expected to accelerate to 4 per cent in 2019, providing grounds for cautious optimism.

|

|

|

Players in the sector must also be mindful of disruptors likely to change the industry. These include rising global demand for liquefied natural gas; the growing prominence of renewables, which could have far-reaching implications; and the potential of the ongoing United States and China trade dispute to disrupt global trade, oil markets and supply chains. Further, digitalization is set to disrupt Africa’s oil and gas sector, where 30 per cent of production stems from legacy fields. The sub-Saharan Africa portfolio of ‘digitally behind’ assets risk becoming obsolete if digitalization is not embraced. This makes the sector ripe for disruption, presenting opportunities for producers and other industry players.

|

There is no universal recipe for winning in the sub-Saharan Africa oil and gas sector. However, soft and hard skills, paired with the right timing, and an understanding of market-specific conditions will bring success. |

|

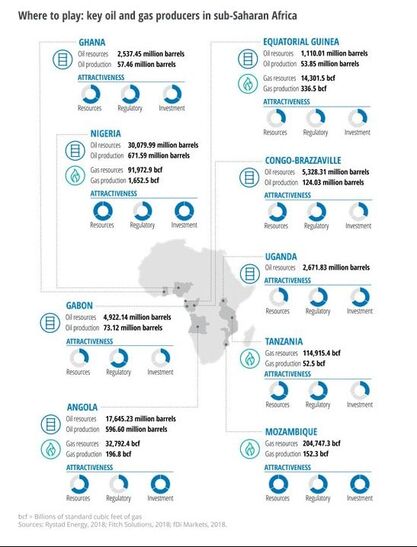

- Congo-Brazzaville joined OPEC in 2018. This, together with a licensing round of 18 blocks (onshore and offshore), could increase investment and reverse declining reserves and production. Production will ramp up in 2019 as projects come online. Refined products consumption has been rising, growing by 28 per cent between 2010 and 2017. This should continue to grow apace with the country’s rapidly increasing population. Refinery capacity is still the main constraint.

- Equatorial Guinea joined OPEC in 2017, but lacks new discoveries and is working maturing oil fields. While oil and gas resources are likely to shrink in the coming decade, the country is still the second-largest producer of natural gas. In May 2018, Equatorial Guinea announced plans to develop a natural gas mega hub linking onshore processing and offshore production facilities. - Crude production has been on the decline in Gabon since 2010. The country re-joined OPEC in 2016 and revamped legislation in the hope of attracting investment, particularly for offshore exploration. These revisions should make licensing and fiscal terms more competitive and flexible. |

|

|

We are the only professional association dedicated to the advancement of abundant, affordable and safe energy.

Our members are solving the world’s greatest energy challenges. |

|

|

2020 © American Energy Society | Terms of Use | Privacy Policy

|