|

Bold ideas that solve the world’s energy needs.

|

Investments in Oil and Gas Set to Soar

|

Bold ideas that solve the world’s energy needs.

|

|

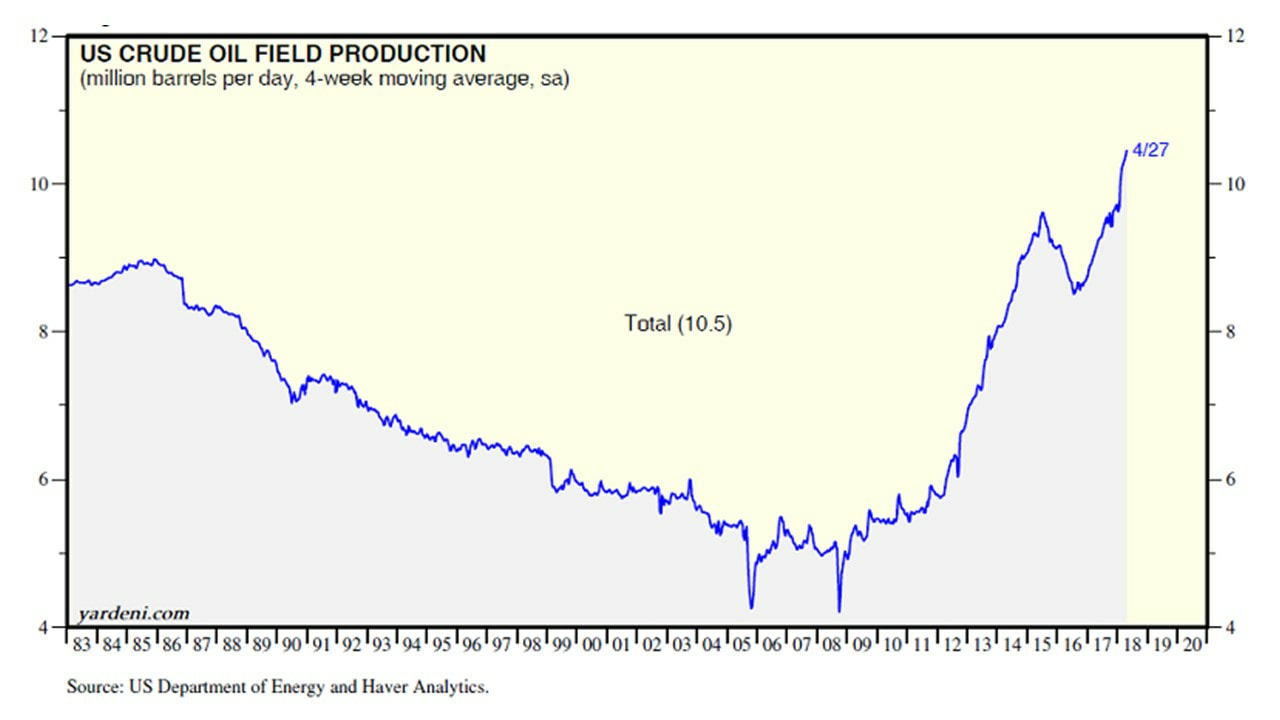

All of this is a perfect scenario for energy investors. The market has rarely been better:

|

|

|

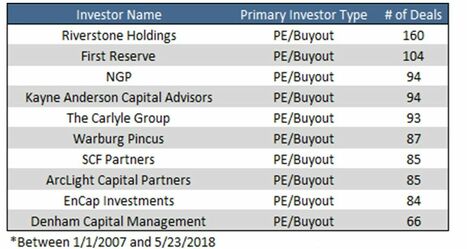

The errors of the public companies creates new opportunities for private energy startups to snap up properties and start drilling. But in order to do that, they need capital right now since this is the moment when US oil production can unilaterally balance world markets. Indeed, Cambridge Associates has long believed in a simple formula: smaller energy-related private equity funds perform better than public energy companies when oil prices are rising.

|

|

|

We are the only professional association dedicated to the advancement of abundant, affordable and safe energy.

Our members are solving the world’s greatest energy challenges. |

|

|

2020 © American Energy Society | Terms of Use | Privacy Policy

|