|

Bold ideas about the world’s energy needs.

|

Myths of Energy Security: It's the Dollars, Not the Barrels

by Michael Lynch

|

Bold ideas about the world’s energy needs.

|

|

The misconception persists, as when during the first Gulf War the Bush Administration (41) argued against releasing oil from the Strategic Petroleum Reserve (SPR) until there were physical shortages. None really occurred because prices balanced the market, just as economic theory predicts. But higher prices (although they didn’t get that high in 1991) were treated as inconsequential, despite the economic damage.

|

"If a major supply disruption were to occur now, when surplus capacity is pretty low, oil prices would soar and the fact that we import very little would mean our import bill would be reduced, but the economy as a whole would still suffer."

|

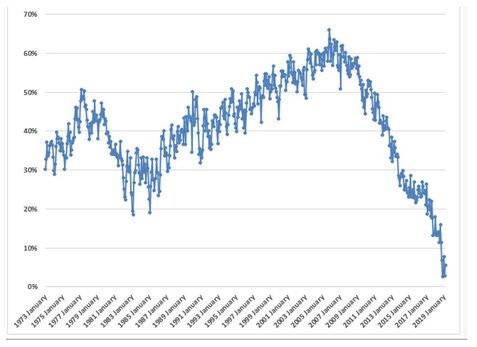

Share of US Oil Consumption Met by Imports

|

If a major supply disruption were to occur now, when surplus capacity is pretty low, oil prices would soar and the fact that we import very little would mean our import bill would be reduced, but the economy as a whole would still suffer. The industry and the Southwest would benefit greatly, but most other consumers would have much less money. A 50% increase in gasoline prices would take about $130 billion out of consumers’ pockets, wiping out the recent tax cuts. Jack Daniels sales might soar, but that wouldn’t do much for the New England economy.

This is not a criticism of the shale industry which has made a huge contribution to the U.S. (and world) economy as well as reducing greenhouse gas emissions more than most countries with green postures. But we shouldn’t think we’re isolated from the world oil market: we’re better off now than when imports passed 60%, but it’s a matter of being safer not safe. |

|

We are the only professional association dedicated to the advancement of abundant, affordable and safe energy.

Our members are solving the world’s greatest energy challenges. |

|

|

2020 © American Energy Society | Terms of Use | Privacy Policy

|